How Much Does It Cost Monthly for a Baby

Learning Outcomes

- Calculate one-time simple interest, and simple involvement over time

- Make up one's mind APY given an interest scenario

- Calculate chemical compound involvement

We take to piece of work with money every day. While balancing your checkbook or calculating your monthly expenditures on espresso requires simply arithmetics, when we start saving, planning for retirement, or need a loan, nosotros need more than mathematics.

Simple Interest

Discussing interest starts with the main, or amount your account starts with. This could be a starting investment, or the starting amount of a loan. Interest, in its nearly elementary form, is calculated as a percent of the principal. For example, if you borrowed $100 from a friend and hold to repay it with five% involvement, and so the amount of interest you would pay would just exist 5% of 100: $100(0.05) = $5. The full amount y'all would repay would be $105, the original principal plus the interest.

Simple One-fourth dimension Interest

[latex]\begin{align}&I={{P}_{0}}r\\&A={{P}_{0}}+I={{P}_{0}}+{{P}_{0}}r={{P}_{0}}(ane+r)\\\end{align}[/latex]

- I is the interest

- A is the cease amount: principal plus interest

- [latex]\begin{align}{{P}_{0}}\\\end{align}[/latex] is the primary (starting amount)

- r is the interest rate (in decimal course. Instance: five% = 0.05)

Examples

A friend asks to borrow $300 and agrees to repay it in thirty days with iii% interest. How much interest will yous earn?

The post-obit video works through this example in detail.

One-time simple interest is merely common for extremely short-term loans. For longer term loans, it is common for interest to exist paid on a daily, monthly, quarterly, or almanac footing. In that example, interest would be earned regularly.

For example, bonds are essentially a loan fabricated to the bond issuer (a company or regime) by you, the bond holder. In return for the loan, the issuer agrees to pay involvement, ofttimes annually. Bonds have a maturity date, at which time the issuer pays dorsum the original bond value.

Exercises

Suppose your city is building a new park, and issues bonds to raise the money to build information technology. Y'all obtain a $1,000 bond that pays v% interest annually that matures in 5 years. How much involvement will you earn?

Show Solution

Each yr, you would earn 5% interest: $g(0.05) = $50 in interest. And so over the course of 5 years, you would earn a total of $250 in interest. When the bond matures, you would receive back the $1,000 you lot originally paid, leaving yous with a total of $1,250.

Further explanation about solving this example can exist seen here.

We tin can generalize this idea of uncomplicated interest over fourth dimension.

Uncomplicated Interest over Fourth dimension

[latex]\begin{marshal}&I={{P}_{0}}rt\\&A={{P}_{0}}+I={{P}_{0}}+{{P}_{0}}rt={{P}_{0}}(1+rt)\\\cease{align}[/latex]

- I is the interest

- A is the end amount: primary plus interest

- [latex]\begin{align}{{P}_{0}}\\\finish{align}[/latex] is the principal (starting amount)

- r is the interest rate in decimal form

- t is time

The units of measurement (years, months, etc.) for the time should match the fourth dimension period for the interest rate.

APR – Annual Percent Rate

Interest rates are usually given every bit an almanac percentage charge per unit (APR) – the total interest that will be paid in the year. If the interest is paid in smaller time increments, the Apr will be divided upwardly.

For instance, a 6% APR paid monthly would be divided into twelve 0.5% payments.

[latex]6\div{12}=0.5[/latex]

A 4% annual charge per unit paid quarterly would be divided into 4 1% payments.

[latex]4\div{4}=ane[/latex]

Instance

Treasury Notes (T-notes) are bonds issued by the federal authorities to cover its expenses. Suppose you obtain a $1,000 T-note with a 4% annual charge per unit, paid semi-annually, with a maturity in 4 years. How much interest will you earn?

This video explains the solution.

Try It

Try It

A loan company charges $thirty involvement for a one calendar month loan of $500. Observe the annual interest rate they are charging.

Try It

Compound Interest

With simple interest, nosotros were assuming that we pocketed the involvement when we received it. In a standard bank account, any interest we earn is automatically added to our balance, and nosotros earn interest on that interest in future years. This reinvestment of involvement is chosen compounding.

Suppose that we eolith $yard in a bank account offering three% interest, compounded monthly. How will our money grow?

The 3% interest is an annual percentage charge per unit (APR) – the full involvement to exist paid during the twelvemonth. Since involvement is beingness paid monthly, each month, we volition earn [latex]\frac{3%}{12}[/latex]= 0.25% per month.

In the commencement month,

- P0 = $m

- r = 0.0025 (0.25%)

- I = $1000 (0.0025) = $2.50

- A = $1000 + $2.l = $1002.50

In the start month, we will earn $ii.50 in involvement, raising our account balance to $1002.50.

In the second month,

- P0 = $1002.50

- I = $1002.50 (0.0025) = $two.51 (rounded)

- A = $1002.50 + $2.51 = $1005.01

Discover that in the second month we earned more involvement than we did in the first month. This is because we earned involvement non only on the original $grand nosotros deposited, merely nosotros also earned interest on the $2.fifty of interest we earned the commencement month. This is the primal advantage that compounding involvement gives us.

Calculating out a few more months gives the following:

| Month | Starting residue | Interest earned | Ending Balance |

| ane | yard.00 | ii.50 | 1002.fifty |

| 2 | 1002.50 | 2.51 | 1005.01 |

| 3 | 1005.01 | 2.51 | 1007.52 |

| four | 1007.52 | 2.52 | 1010.04 |

| 5 | 1010.04 | two.53 | 1012.57 |

| 6 | 1012.57 | 2.53 | 1015.10 |

| 7 | 1015.ten | 2.54 | 1017.64 |

| eight | 1017.64 | 2.54 | 1020.18 |

| 9 | 1020.eighteen | 2.55 | 1022.73 |

| 10 | 1022.73 | 2.56 | 1025.29 |

| 11 | 1025.29 | 2.56 | 1027.85 |

| 12 | 1027.85 | 2.57 | 1030.42 |

We want to simplify the process for calculating compounding, considering creating a table like the i above is time consuming. Luckily, math is skilful at giving you ways to have shortcuts. To find an equation to represent this, if Pg represents the amount of coin after m months, so nosotros could write the recursive equation:

P0 = $thousand

Pm = (1+0.0025)Pm-i

Y'all probably recognize this as the recursive class of exponential growth. If not, we go through the steps to build an explicit equation for the growth in the next example.

Case

Build an explicit equation for the growth of $1000 deposited in a banking concern business relationship offering 3% interest, compounded monthly.

View this video for a walkthrough of the concept of compound involvement.

While this formula works fine, information technology is more than common to use a formula that involves the number of years, rather than the number of compounding periods. If Due north is the number of years, then m = N k. Making this change gives united states the standard formula for compound interest.

Compound Interest

[latex]P_{N}=P_{0}\left(1+\frac{r}{k}\right)^{Nk}[/latex]

- PN is the balance in the account after N years.

- P0 is the starting balance of the account (also called initial deposit, or principal)

- r is the annual interest rate in decimal class

- k is the number of compounding periods in ane year

- If the compounding is washed annually (once a year), k = 1.

- If the compounding is washed quarterly, m = iv.

- If the compounding is washed monthly, k = 12.

- If the compounding is washed daily, k = 365.

The near of import affair to remember about using this formula is that it assumes that we put coin in the account once and let it sit down there earning involvement.

In the side by side example, we testify how to use the compound interest formula to discover the balance on a certificate of deposit subsequently twenty years.

Example

A certificate of deposit (CD) is a savings musical instrument that many banks offering. It commonly gives a higher interest rate, but you cannot access your investment for a specified length of fourth dimension. Suppose you deposit $3000 in a CD paying half-dozen% interest, compounded monthly. How much will you accept in the account subsequently 20 years?

A video walkthrough of this instance problem is available below.

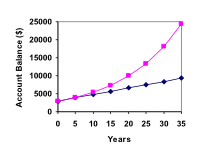

Let us compare the corporeality of money earned from compounding confronting the amount you lot would earn from uncomplicated interest

| Years | Elementary Interest ($fifteen per month) | 6% compounded monthly = 0.5% each month. |

| five | $3900 | $4046.55 |

| 10 | $4800 | $5458.19 |

| 15 | $5700 | $7362.28 |

| xx | $6600 | $9930.61 |

| 25 | $7500 | $13394.91 |

| 30 | $8400 | $18067.73 |

| 35 | $9300 | $24370.65 |

As yous can see, over a long period of time, compounding makes a big departure in the account balance. Y'all may recognize this as the difference between linear growth and exponential growth.

Attempt It

Evaluating exponents on the calculator

When we need to calculate something like [latex]5^three[/latex] it is piece of cake enough to just multiply [latex]5\cdot{5}\cdot{five}=125[/latex]. But when we need to calculate something similar [latex]i.005^{240}[/latex], information technology would be very dull to summate this by multiplying [latex]1.005[/latex] by itself [latex]240[/latex] times! Then to make things easier, we can harness the power of our scientific calculators.

Most scientific calculators have a button for exponents. It is typically either labeled similar:

^ , [latex]y^ten[/latex] , or [latex]x^y[/latex] .

To evaluate [latex]1.005^{240}[/latex] we'd type [latex]1.005[/latex] ^ [latex]240[/latex], or [latex]i.005 \space{y^{x}}\space 240[/latex]. Try information technology out – y'all should get something effectually 3.3102044758.

Example

You know that yous will need $xl,000 for your child'due south education in 18 years. If your account earns 4% compounded quarterly, how much would y'all need to deposit now to reach your goal?

Try It

Rounding

It is important to be very conscientious about rounding when calculating things with exponents. In general, you lot want to continue as many decimals during calculations as y'all can. Be sure to keep at least 3 meaning digits (numbers afterward any leading zeros). Rounding 0.00012345 to 0.000123 will usually give you lot a "close enough" answer, merely keeping more than digits is always ameliorate.

Example

To run into why not over-rounding is and then important, suppose you lot were investing $1000 at 5% involvement compounded monthly for xxx years.

| P0 = $1000 | the initial deposit |

| r = 0.05 | v% |

| k = 12 | 12 months in 1 year |

| North = thirty | since we're looking for the amount later on xxx years |

If nosotros first compute r/k, we find 0.05/12 = 0.00416666666667

Hither is the event of rounding this to different values:

| r/k rounded to: | Gives P30 to be: | Error |

| 0.004 | $4208.59 | $259.15 |

| 0.0042 | $4521.45 | $53.71 |

| 0.00417 | $4473.09 | $v.35 |

| 0.004167 | $4468.28 | $0.54 |

| 0.0041667 | $4467.lxxx | $0.06 |

| no rounding | $4467.74 |

If you're working in a banking concern, of course you wouldn't round at all. For our purposes, the answer we got by rounding to 0.00417, three meaning digits, is close plenty – $v off of $4500 isn't too bad. Certainly keeping that quaternary decimal identify wouldn't have injure.

View the post-obit for a demonstration of this example.

Using your reckoner

In many cases, yous tin avoid rounding completely past how you enter things in your computer. For example, in the example in a higher place, we needed to calculate [latex]{{P}_{xxx}}=1000{{\left(ane+\frac{0.05}{12}\right)}^{12\times30}}[/latex]

We can quickly calculate 12×30 = 360, giving [latex]{{P}_{30}}=1000{{\left(1+\frac{0.05}{12}\right)}^{360}}[/latex].

Now we can use the calculator.

| Type this | Calculator shows |

| 0.05 ÷ 12 = . | 0.00416666666667 |

| + one = . | 1.00416666666667 |

| yx 360 = . | iv.46774431400613 |

| × one thousand = . | 4467.74431400613 |

Using your reckoner continued

The previous steps were assuming you accept a "one operation at a time" calculator; a more than avant-garde reckoner will frequently allow you to type in the entire expression to be evaluated. If you have a figurer like this, you volition probably just need to enter:

1000 × ( ane + 0.05 ÷ 12 ) y10 360 =

Solving For Time

Note: This section assumes yous've covered solving exponential equations using logarithms, either in prior classes or in the growth models affiliate.

Often nosotros are interested in how long information technology volition have to accumulate money or how long we'd demand to extend a loan to bring payments down to a reasonable level.

Examples

If yous invest $2000 at 6% compounded monthly, how long will it take the account to double in value?

Get additional guidance for this example in the post-obit:

How Much Does It Cost Monthly for a Baby

Source: https://courses.lumenlearning.com/wmopen-mathforliberalarts/chapter/introduction-how-interest-is-calculated/

0 Response to "How Much Does It Cost Monthly for a Baby"

Postar um comentário